Again, this will be year of two markets. The first half will be slow, with prices dropping by a further 2-3% on average. When mortgage rates start to fall, not all buyers will re-enter the market, as some will wait for rates to fall further.

Again, this will be year of two markets. The first half will be slow, with prices dropping by a further 2-3% on average. When mortgage rates start to fall, not all buyers will re-enter the market, as some will wait for rates to fall further. Five Year fixed-rate mortgages are currently at 5.6%. Expect these rates to end 2024 at 4.5%. Variable rate mortgages are currently at 7%, bu should also drop to 4.25%.

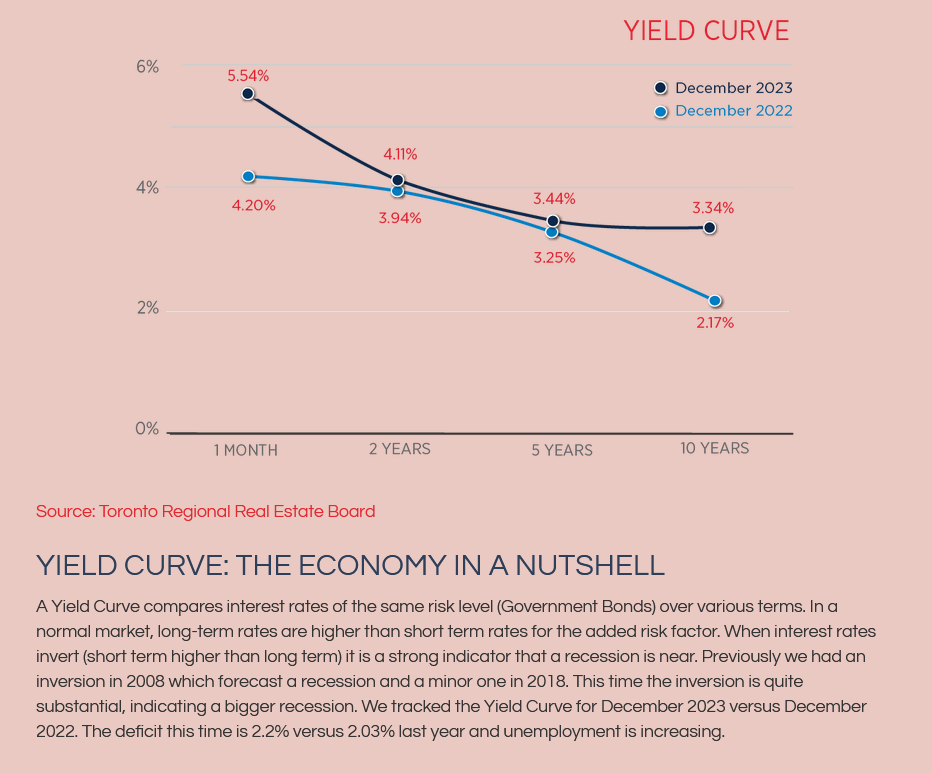

Five Year fixed-rate mortgages are currently at 5.6%. Expect these rates to end 2024 at 4.5%. Variable rate mortgages are currently at 7%, bu should also drop to 4.25%. Unemployment is now at 5.8% (it was 4.5% in 2022). We are heading into a recession. Just look at our Yield curve from year-end to 2022 to the current one.

Unemployment is now at 5.8% (it was 4.5% in 2022). We are heading into a recession. Just look at our Yield curve from year-end to 2022 to the current one. Continued population growth of one million people a year (500,000 immigrants and the rest refugees and international students) will increase the demand for housing. 50% of these people are coming to Ontario.

Continued population growth of one million people a year (500,000 immigrants and the rest refugees and international students) will increase the demand for housing. 50% of these people are coming to Ontario. Housing completions are averaging 220,000 per year and Ontario makes up only 35% of this total.

Housing completions are averaging 220,000 per year and Ontario makes up only 35% of this total. Don’t expect a surplus of listings from sellers to solve the housing shortage. The Mortgage arears (over 3 months) number in Ontario is higher (.10%) than the last two years, but it represents only 2200 houses in total.

Don’t expect a surplus of listings from sellers to solve the housing shortage. The Mortgage arears (over 3 months) number in Ontario is higher (.10%) than the last two years, but it represents only 2200 houses in total. Don’t hold your breath for ‘affordable housing’ to have any impact in 2024. Government over promises and under delivers (think Eglinton LRT Crosstown). The only way to get ‘affordable housing’ is for governments to buy housing at market prices/costs. Then sell or rent them out at 50% below market and pay for it through government deficits.

Don’t hold your breath for ‘affordable housing’ to have any impact in 2024. Government over promises and under delivers (think Eglinton LRT Crosstown). The only way to get ‘affordable housing’ is for governments to buy housing at market prices/costs. Then sell or rent them out at 50% below market and pay for it through government deficits.

Victor Alvarez, Sales Representative

Mobile: 647-223-0562

Phone: 416-203-6636

Fax: 416-203-1908

RE/MAX Condos Plus Corp. Brokerage

45 Harbour Square Toronto, ON M5J 2G4

![]()